Round Up to Save®

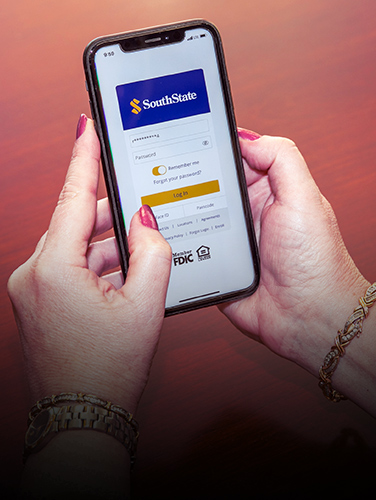

Welcome to Banking Forward

The journey to reaching your financial goals starts here.

Get a $200 Head Start

Open a personal checking account, and you can earn $200. That’s a good start.

Get Started

Manage Your Debit Card Your Way

At home or on the go, you can now control your SouthState debit card(s) in our mobile banking app.

Get Started

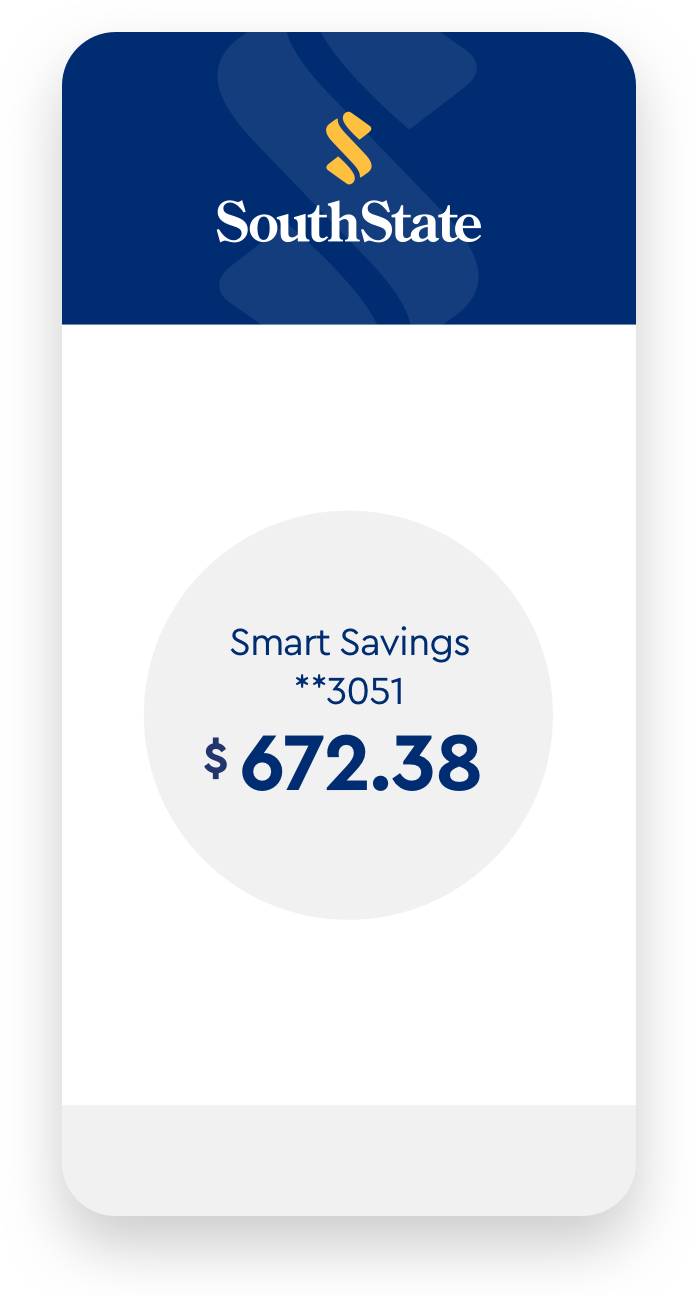

Spring Forward with Round Up to Save®

Time to let your finances bloom! Use Round Up to Save and watch your savings grow this season.

Start Saving

SouthState Releases Corporate Social Responsibility Report

Annual report demonstrates our commitment to stakeholders.

Learn More

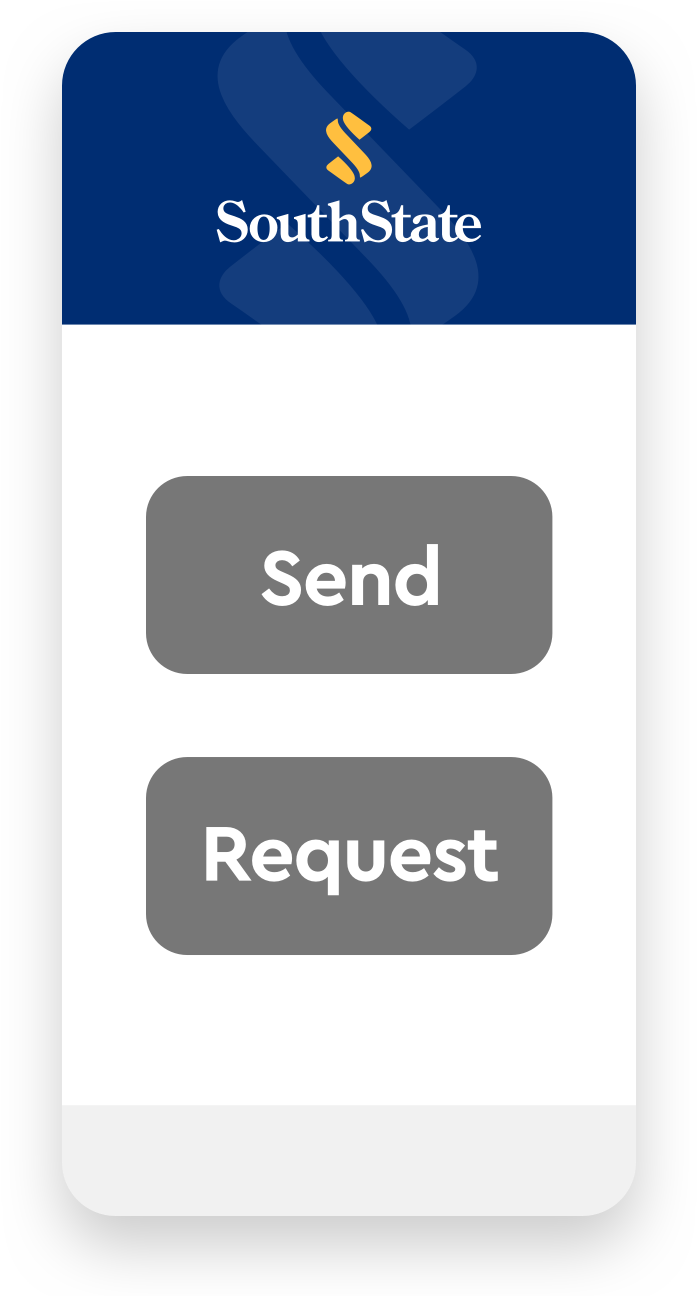

Send Money With Zelle®

A fast, safe and easy way to send money directly from your bank account to another’s.

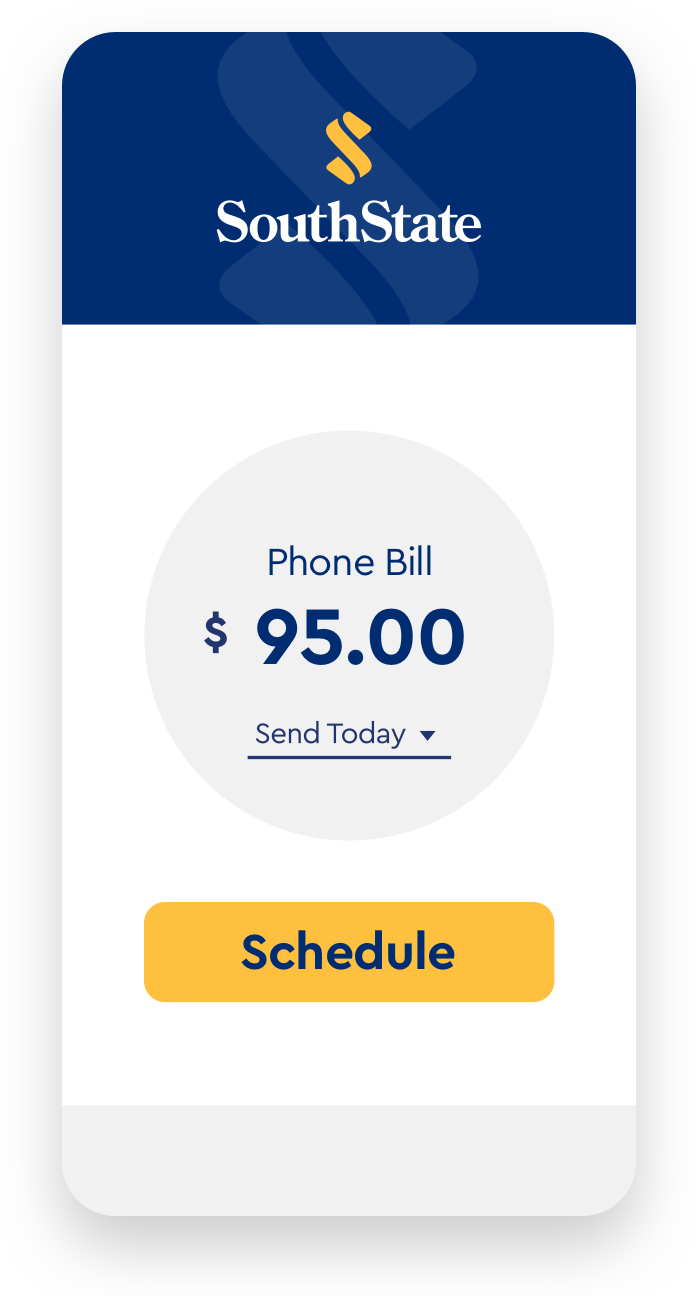

Pay Your Bills

Pay all your bills in one place and set up automatic payments to save time.

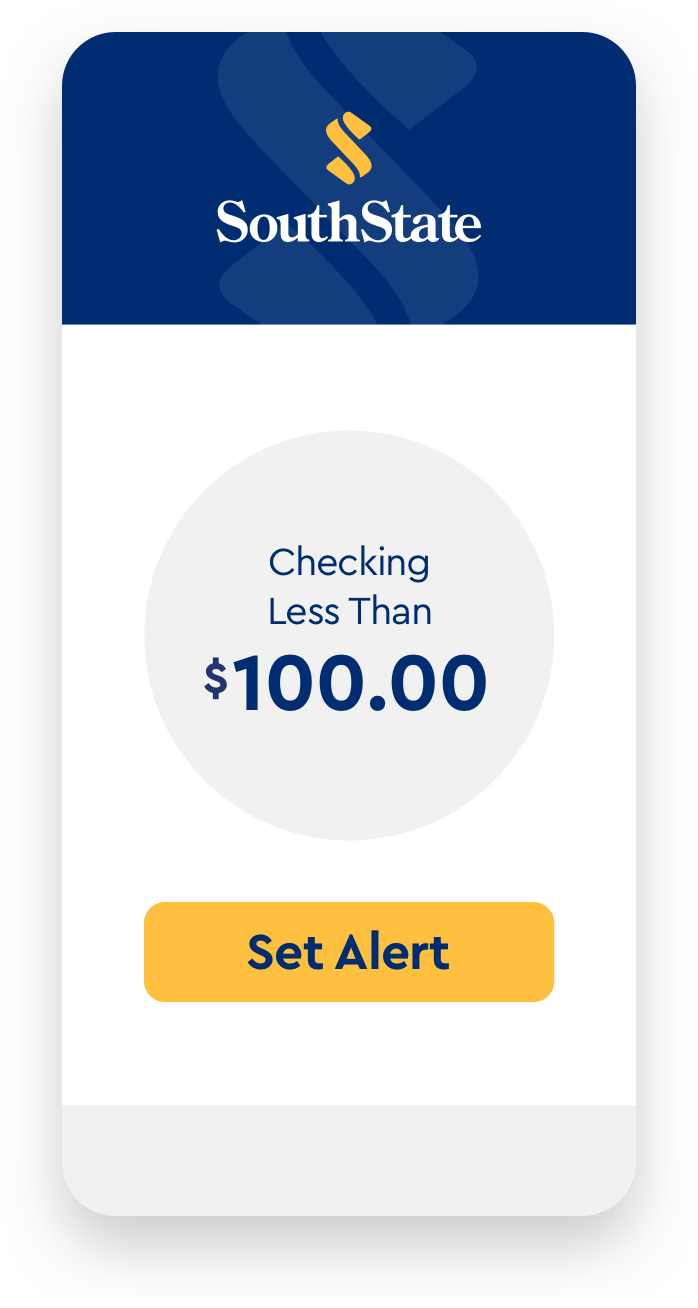

Get Alerts

Updated alerts let you create customized alerts that can be sent as a push notification or secure message.

Instant Info

Know your account information immediately with smart watch integration.2

Better Rates to Help You Reach Your Goals

Stories and Insights

-

Zelle and the Zelle related marks are wholly owned by Early Warning Services, LLC and are used herein under license.

Transactions typically occur in minutes when the recipient’s email address or U.S. mobile number is already enrolled with Zelle. - Apple Watch is a trademark of Apple, Inc. and Apple is a registered trademark of Apple, Inc.

- Annual Percentage Rate (APR) is accurate as of 04/15/2024 and includes a one-time $150 loan origination fee and 0.50% interest rate discount for automatic payment draft from a SouthState checking account. Minimum loan amount $4,000; maximum loan amount $150,000. 6.83% APR is based on an example loan amount of $40,000 for a term of 72 months with monthly payments of $676.19. Additional fees may apply. Other restrictions may apply. Your actual APR may vary based on creditworthiness, loan amount, loan term and vehicle. Rates, terms and conditions are subject to change based on borrower eligibility and market conditions. All loans are subject to credit approval.

- Annual Percentage Rate (APR) is accurate as of 10/23/2023 and includes a one-time $150 loan origination fee and 0.50% interest rate discount for automatic payment draft from a SouthState checking account. Minimum loan amount $5,000; maximum loan amount $300,000. 7.79% APR is based on an example loan amount of $70,000 for a term of 144 months with monthly payments of $748.16. 144 month term available for a loan amount of $50,000 - $74,999. Additional fees may apply. Other restrictions may apply. Your actual APR may vary based on creditworthiness, loan amount, loan term and collateral. Other rates and terms available. Rates, terms and conditions offered are subject to change without notice. All loans are subject to credit approval.

- Annual Percentage Rate (APR) is accurate as of 10/23/2023 and includes a one-time $150 loan origination fee and 0.50% interest rate discount for automatic payment draft from a SouthState checking account. Minimum loan amount $4,000; maximum loan amount $50,000. 7.14% APR is based on an example loan amount of $40,000 for a term of 72 months with monthly payments of $682.11. Additional fees may apply. Other restrictions may apply. Your actual APR may vary based on creditworthiness, loan amount, loan term and vehicle. Rates, terms and conditions offered are subject to change without notice. All loans are subject to credit approval.